Every so often a company reports a genuinely great quarter and the stock falls anyway, and everyone reaches for the same lazy explanation: "priced for perfection."

That explanation is almost always wrong, or at least incomplete.

What happened to TSMC on Thursday is a much more interesting story about who actually gets paid when a boom happens, and who just gets to build it.

Is being indispensable to history's biggest infrastructure buildout the same thing as profiting from it? Let’s find out.

But before we get to that, let's take a quick look at the markets and what matters today…

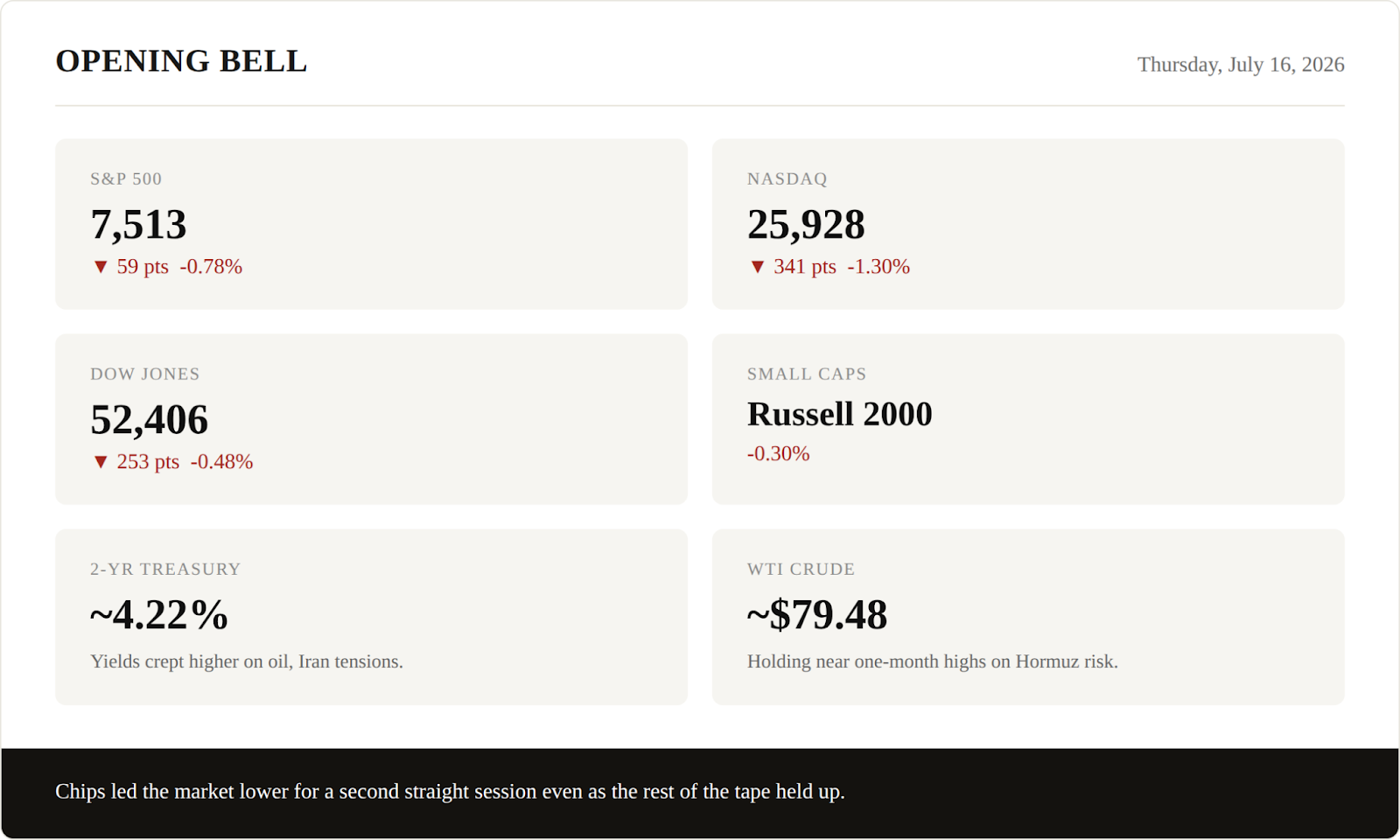

3 Movers in 3 Minutes

- Netflix's guidance gap. Netflix (NFLX) dropped nearly 9% after the bell as its Q2 report matched estimates but investors focused on where growth goes once price hikes and password-sharing cleanup fully cycle through the base. Full-year guidance held at $50.7 to $51.7 billion in revenue, which wasn't the problem. The problem was that nothing in the update gave the market a new reason to pay 24 times earnings for a maturing subscription business.

- UnitedHealth's rare good quarter. UnitedHealth Group (UNH) jumped as much as 8.7% after posting adjusted earnings of $6.38 a share against estimates near $4.90, and raising its full-year outlook to $19.50 to $20 a share. Its medical cost ratio, the share of premiums it pays out in claims, improved to 86.7% from 89.4% a year ago. After eighteen months of the insurer explaining away cost overruns, one clean quarter was worth a near double-digit pop.

- A $2.8 billion bet on mushrooms of the mind. Eli Lilly (LLY) agreed to buy psychedelic drugmaker AtaiBeckley for $6.75 a share in cash plus up to $2.50 in milestone payments, and shares of the target more than doubled intraday. The deal is a quiet marker of how fast psychedelic medicine has gone from Berkeley basement research to a line item on a Big Pharma balance sheet.

3 Signals for Today

- Housing Starts, 8:30 AM. June's reading lands with 30-year mortgage rates near 6.55%, their highest in nearly a year, a real test of whether homebuilders are still willing to break ground into higher financing costs.

- Industrial Production & Capacity Utilization, 9:15 AM. With the chip sector's capex debate front and center, today's factory-output data is the closest thing to a scorecard on whether the broader economy is actually absorbing all that new capacity.

- Michigan Consumer Sentiment (Preliminary), 10 AM. The first read on how households are feeling in July, arriving just two days after inflation data came in soft and one day after oil prices ticked back up.

Warren Buffett Once Passed on Amazon

"I was too dumb to realize it. I did not think Bezos could succeed on the scale he has."

By the time most people saw what Amazon was doing to retail, it was too late to get in early.

History is offering a second chance.

Mode Mobile is doing to the $1T+ smartphone industry what Amazon did to retail — turning everyday phones into money-making machines.

The traction is already there:

- 490M+ users earning passive income from their phones

- $1B+ saved and earned by users worldwide

- 32,481% revenue growth — Deloitte's #1 fastest-growing software company

- $115M+ in revenue and climbing

People spend 30+ hours a week on their phones. Mode figured out how to monetize that time and pay users directly.

They've secured the $MODE ticker from Nasdaq — signaling plans to go public soon.

Unlike Amazon, you can still get in early…

Tap into a $1T opportunity — invest now at just $0.52/share and get up to 20% bonus!

Disclaimer: Please read the offering circular and related risks at invest.modemobile.com. This is a paid advertisement for Mode Mobile’s Regulation A+ Offering. Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur. The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period.

And with that out of the way, let's get to today's big story: what it means when a company's best quarter in its history is the thing that spooks investors.

The Sip

In the late 1990s, telecom companies laid enough fiber optic cable to circle the Earth more than a thousand times over.

They did this on a bet. The internet was coming, traffic would explode, and whoever owned the infrastructure would own the future.

They were right about the traffic. Global Crossing alone spent close to $20 billion building a fiber network across oceans and continents, certain that demand would eventually catch up to capacity.

And it did. Just not on their timeline, and not in a way that paid them back.

By 2002, Global Crossing was bankrupt. So were dozens of other carriers who had built the exact infrastructure the internet needed. The fiber didn't go to waste. Google (GOOGL), Amazon (AMZN) and Netflix eventually lit up that same glass at a fraction of what it cost to lay, because bankruptcy auctions are a wonderful thing if you're the buyer.

So the people who built the boom weren't the people who got paid by it.

Which brings us to Thursday, and to Taiwan Semiconductor Manufacturing Company (TSM), and to one of the stranger scenes in this earnings season.

Because TSMC posted the best quarter in its history. Revenue hit a record $40.2 billion, up nearly 34% from a year ago. Net profit surged 77%. Gross margin came in at 67.7%. Management raised its full-year growth forecast, again, for the second time this year.

TSMC shares fell more than 4% before the opening bell.

Except this isn't a story about disappointment. Nobody on the call disputed the numbers. What they disputed was the bill.

You see, TSMC's 2026 capital budget sits between $52 and $56 billion, roughly 37% above last year and the largest in the company's history, with management signaling it intends to spend at the top of that range. That is not incremental but TSMC is committing more money to new fabs in a single year than most S&P 500 companies are worth.

And here's the tension.

A foundry operates on 18 to 24 month planning cycles. Every dollar TSMC commits today is a wager on where AI chip demand sits two or three years from now, not next quarter. If that demand shows up as forecast, the new capacity prints money for a decade. If it pauses, even briefly, TSMC is left holding depreciation on factories built for a future that arrived late, or not at all.

World's Largest Investors Are Moving Their Money (Not Into AI)

While the media distracts you with stories about the next big AI IPO... The world's largest investors are moving their money into one asset – at the fastest pace in a generation. This asset has crushed the S&P 500's return over the past 12 months… More than TRIPLED the S&P 500's return in 2025… and has outperformed the S&P 500 over the past 25 years by more than 1,100 percentage points. According to one Wall Street veteran, with over 40 years of professional investing experience… the biggest gains could be still ahead. That's why he's urging you to make one money move now.

This ad is sent on behalf of Stansberry Research, 1125 N Charles St, Baltimore, MD 21201. If you would like to optout from receiving offers from Stansberry Research please click here.

And the customer math makes that risk sharper than it looks. TSMC's ten largest customers generate 78% of its revenue, with a single customer, almost certainly Nvidia (NVDA) by way of its advanced packaging orders, accounting for roughly 19% on its own. One analyst put the market's real anxiety plainly: rising capex is usually a signal to fade a cyclical business, not chase it.

So you have to notice what TSMC actually is. When Morris Chang founded the company in 1987, the entire premise was that TSMC would never design its own chips, only manufacture other people's. It was a bet that being the indispensable middleman was safer than picking winners in any single product cycle. For almost forty years, that bet worked beautifully, because TSMC never had to carry the demand risk of any one customer's success or failure.

The AI era has quietly broken that insulation.

When 78% of your revenue rides on ten customers, and roughly a fifth of it rides on one, you are no longer just the neutral manufacturer sitting above the fray. You are exposed to the same concentrated bet your biggest customer is making, just one supply-chain link removed. The semiconductor sector's broader benchmark, the Philadelphia SE Semiconductor index, fell almost 4% the same day on that exact realization, dragging Nvidia, AMD, Micron (MU) and Intel (INTC) down alongside TSMC even though none of them had reported anything.

That's the reframe.

TSMC isn't being punished for a bad quarter. It's being re-priced from "the irreplaceable king of AI chips" to "the biggest capital-intensity bet in the AI trade," and those are two very different stocks trading at two very different multiples, even when the revenue line looks identical.

Being essential to a boom and profiting from a boom are not the same claim. Global Crossing was essential to the internet. It still went bankrupt building it.

The stock still requires investors to believe that extraordinary AI spending will remain extraordinary.

That's the whole bet, stated plainly. Not whether AI demand exists. Whether it stays extraordinary long enough to make today's factory bill look cheap in hindsight rather than reckless.

He predicted the 2008 financial crisis…

He predicted Trump’s election in 2016….

He even predicted the rise of COVID-19 writing:

“The chance we don’t have something on the scale of a national pandemic in the next few years is near zero”

That was three months before the first reported case.

If he’s right again, God Bless America…

Because this crisis will be tectonic in scale…and it's going to begin with the bubble popping in AI.

The Long Angle

This mechanic shows up everywhere capital gets deployed years ahead of demand.

Railroads laid more track across the American West in the 1870s and 1880s than freight volumes justified for a generation, and half the companies that built those lines went through bankruptcy before the traffic caught up. Shale drillers in the 2010s borrowed heavily to drill wells on the promise of oil prices that didn't always cooperate, and the equity holders who financed the boom rarely captured what the eventual consolidators did.

The pattern is always the same. Whoever builds the infrastructure takes the cyclical risk up front. Whoever uses the infrastructure later gets the economics once the risk has already been underwritten by someone else's balance sheet.

That doesn't mean TSMC is Global Crossing.

TSMC is wildly profitable, structurally dominant, and probably right about where AI demand is heading. But ‘probably right’ and ‘certain enough to justify today's price’ are different bars, and Thursday's selloff was the market quietly admitting it can no longer tell the difference.

The chips are real. The demand is real. What's being repriced is simply how much anyone should pay today for a bet that only pays off if tomorrow behaves exactly as promised.

The MarketSips Takeaway

The next time a picks and shovels stock looks like the safe way to play a boom, ask who actually owns the risk in that trade.

Infrastructure builders don't get to opt out of the cycle just because they're indispensable to it. They just experience the cycle differently, usually through the capex line rather than the revenue line, and usually a year or two before anyone else notices.

Today's reply prompt: Would you rather own the company building the AI boom, or the companies simply renting its output?

Until then, sip slowly!

The Market Sip Desk